You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

CX-5 0% APR - Loan Origination Fee?

- Thread starter NWDriver

- Start date

cz5gt

CX-5 GT

First time I hear about loan origination fee. Isnt this more related to mortgages vs car finance loan?

There is usually a return fee if its lease , if its finance no fees I think.i.e No hidden fees by the captive lender for the loan. You can get up to 62 or 63 months at the 0%. 72mo is also dirt cheap now , like less than 2%. Good subsidy by Mazda this month.

What the dealer does is another story.

There is usually a return fee if its lease , if its finance no fees I think.i.e No hidden fees by the captive lender for the loan. You can get up to 62 or 63 months at the 0%. 72mo is also dirt cheap now , like less than 2%. Good subsidy by Mazda this month.

What the dealer does is another story.

- :

- 2021 CX-9 Sig

- :

- 2021 CX-5 GT

Mazda looks to have sold over 20K CX-5 in December. That low APR did its job!

www.prnewswire.com

www.prnewswire.com

Mazda Reports Record December Sales and Full-Year 2023 Sales Results

/PRNewswire/ -- Mazda North American Operations (MNAO) today reported total December sales of 39,518 vehicles, an increase of 44.8 percent compared to December...

Anybody know how long the 0% will last?Mazda looks to have sold over 20K CX-5 in December. That low APR did its job!

Mazda Reports Record December Sales and Full-Year 2023 Sales Results

/PRNewswire/ -- Mazda North American Operations (MNAO) today reported total December sales of 39,518 vehicles, an increase of 44.8 percent compared to December...

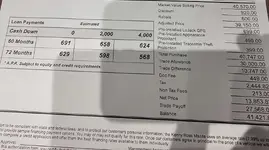

What is the price of the car at 0%, versus the price if paying cash?Premium and higher still have it

0% financing can be a bit of smoke and mirrors, as most dealers raise the price of the car to cover their financing costs. That or they will not negotiate down to the same level if you are paying cash or taking the cash incentive instead of a loan.

Remember, nothing is free, especially a loan. If you think you are getting a loan at 0%, think again.

Somewhere along the way, you are paying interest.

Also, now the 0% is over 36 months not 60 months like before 1/2/24Anybody know how long the 0% will last?

I don't know....a few days ago with walked away with a 0% 60 month loan and got our CX5 Carbon Turbo for 3K less than the dealer was asking!What is the price of the car at 0%, versus the price if paying cash?

0% financing can be a bit of smoke and mirrors, as most dealers raise the price of the car to cover their financing costs. That or they will not negotiate down to the same level if you are paying cash or taking the cash incentive instead of a loan.

Remember, nothing is free, especially a loan. If you think you are getting a loan at 0%, think again.

Somewhere along the way, you are paying interest.

They had the price 2K over MSRP for dealer extras. Knocked that off. Then we negotiated another 1K off the MSRP.

But, they may have made money on our trade...got 18K for our 2018 CX5 with 41K miles but it was not in perfect shape.

Charmer383

2023 CX5 Turbo

I'm going on the 8th for my first oil change. I'm going to get figures on a 24' in same trim. Only change for me would be a white exterior. If I couldn't get the white I'd consider the carbon. When I traded my truck in I had a lot of equity to roll over.

Just_Steve

2024 CX-5 Premium Deep Crystal Blue Mica. New York

I don't believe that's the case at all, I negotiated my price on line and never discussed financing until I sat down with the finance guy. Salesman never had enough information to run my credit, I gave him a credit card deposit $500 over the phone, next day went in spoke to salesman for 5 minutes then dealt with the Finance guy. 0% No smoke, No mirrors.What is the price of the car at 0%, versus the price if paying cash?

0% financing can be a bit of smoke and mirrors, as most dealers raise the price of the car to cover their financing costs. That or they will not negotiate down to the same level if you are paying cash or taking the cash incentive instead of a loan.

Remember, nothing is free, especially a loan. If you think you are getting a loan at 0%, think again.

Somewhere along the way, you are paying interest.

Charmer383

2023 CX5 Turbo

That's one of the key strategies to use when buying a car. Do not tell them how you are paying until the final price has been agreed upon. People that go into a dealer and say that they have a budget of say $450/month (example) are setting themselves up for paying more than they should. Dealers love this.I don't believe that's the case at all, I negotiated my price on line and never discussed financing until I sat down with the finance guy. Salesman never had enough information to run my credit, I gave him a credit card deposit $500 over the phone, next day went in spoke to salesman for 5 minutes then dealt with the Finance guy. 0% No smoke, No mirrors.

I would see this 0% financing advertising in the past, and it would say specifically that you had a choice: 0% financing OR a $3,000 rebate, but not both. In effect, you would be paying $3k more for the car if you decided to finance it. That's not 0% in my books.

Last edited:

I know this a bit of topic, but this brings up a question to me about how to handle the purchase while trading in old car. So do you sort out the tradein first then the purchase price, or the reverse? I get that you don't discuss how you are paying for the car until last but the order of the other two has me confused.That's one of the key strategies to use when buying a car. Do not tell them how you are paying until the final price has been agreed upon. People that go into a dealer and say that they have a budget of say $450/month (example) are setting themselves up for paying more than they should. Dealers love this.

I would see this 0% financing advertising in the past, and it would say specifically that you had a choice: 0% financing OR a $3,000 rebate, but not both. In effect, you would be paying $3k more for the car if you decided to finance it. That's not 0% in my books.

1

172499

In the past I have negotiated the trade in value then negotiated the price of the new car. Both prices have to meet my target price, otherwise there is no deal, and I move on to another dealer.I know this a bit of topic, but this brings up a question to me about how to handle the purchase while trading in old car. So do you sort out the tradein first then the purchase price, or the reverse? I get that you don't discuss how you are paying for the car until last but the order of the other two has me confused.

Last edited by a moderator:

- :

- South Carolina

- :

- 21 CX-9 13 CX-5

Simple answer: never trade in your old car. They will only give you wholesale auction price for it. If you sell it yourself, you will get THOUSANDS of dollars more. Literally thousands.I know this a bit of topic, but this brings up a question to me about how to handle the purchase while trading in old car.

- :

- ‘25 CX-5 SIGNATURE

'24 MX-5 RF GT

Yep, that's the only way to do it. Start with their out-the-door price, then negotiate down from there. It helps to have other options when you next bring up your trade-in so you can get as much as possible if that's your plan. Of course you'll net more if you sell it yourself but that's not something most people are willing to do. Mazda's recent low APRs are hard to beat and between the 0% and CX-5's popularity it's no wonder sales are strong.I don't believe that's the case at all, I negotiated my price on line and never discussed financing until I sat down with the finance guy. Salesman never had enough information to run my credit, I gave him a credit card deposit $500 over the phone, next day went in spoke to salesman for 5 minutes then dealt with the Finance guy. 0% No smoke, No mirrors.

Last edited:

- :

- South Carolina

- :

- 21 CX-9 13 CX-5

Of course you'll net more if you sell it yourself but that's not something most people are willing to do.

But why not? Selling cars is beyond easy. Take some pictures and throw them on FB Marketplace. That's literally all it takes.

Are you saying people are so lazy they are willing to give up thousands and thousands of dollars? I thought they just traded cars because they simply didn't know any better.

New Posts and Comments

- Replies

- 42

- Views

- 50K

- Replies

- 147

- Views

- 16K

- Replies

- 1

- Views

- 133